Tracking investment performance is crucial for making well-informed financial decisions. In India, investors commonly rely on two key metrics to evaluate investment returns: Extended Internal Rate of Return (XIRR) and Compound Annual Growth Rate (CAGR). These metrics help measure the profitability of various asset classes, including mutual funds, stocks, and real estate. While both serve as indicators of investment performance, they cater to different financial scenarios.

Understanding the difference between XIRR and CAGR is essential for selecting the appropriate metric for financial analysis, particularly in the Indian investment landscape. This article provides a detailed comparison of XIRR and CAGR, along with examples relevant to Indian investors.

What is XIRR?

Definition of XIRR

Extended Internal Rate of Return (XIRR) is a financial metric that calculates the annualized return on investments involving multiple cash inflows and outflows at different intervals. Unlike CAGR, which assumes a fixed growth rate over time, XIRR accounts for the exact timing and amount of each transaction.

Importance of XIRR in India

XIRR is particularly beneficial in evaluating investment avenues where cash flows occur at different times. Some common Indian investment scenarios where XIRR is relevant include:

Systematic Investment Plans (SIPs) in mutual funds – Investors contribute fixed amounts at regular intervals.

Real estate investments – Payments and returns occur at different times in phased development projects.

Stock market investments – Shares are bought and sold at different intervals rather than a one-time lump sum investment.

Recurring deposits and fixed deposits with periodic additions – Investors add funds at different times rather than in one go.

Since these types of investments involve staggered contributions and withdrawals, using a simple CAGR formula may not accurately represent actual returns.

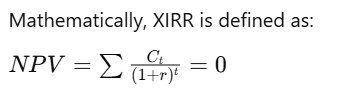

Formula for XIRR Calculation

Where:

NPV (Net Present Value) is the sum of all cash flows, discounted to the present value.

C_t represents the cash flow at time t.

r is the internal rate of return that sets NPV to zero.

Since solving for r manually is complex, investors typically use Excel’s XIRR function or online financial calculators.

Example of XIRR Calculation

Assume an Indian investor contributes ₹5000 monthly to a SIP for three years. By the end of three years, the total investment amounts to ₹1.8 lakh, and the portfolio is valued at ₹2.5 lakh. Since each installment is invested at a different time, each contribution has a different duration to grow. Using XIRR, the investor can accurately determine their annualized return, reflecting the effect of varying investment durations.

What is CAGR?

Definition of CAGR

Compound Annual Growth Rate (CAGR) is a measure of an investment’s annual growth rate, assuming a constant rate of return over a specified period. It is particularly useful for analyzing investments where a lump sum is invested and left to grow over time.

Importance of CAGR in India

CAGR is widely used for evaluating:

Lump sum investments in mutual funds and stocks – Investors invest a fixed amount and let it grow.

Fixed deposits (FDs) and bonds – These offer predictable, steady returns.

Long-term investments such as Public Provident Fund (PPF) or National Pension System (NPS) – Investors track annualized returns over time.

Since CAGR provides a smoothed-out average growth rate, it allows investors to compare different investments easily.

Where:

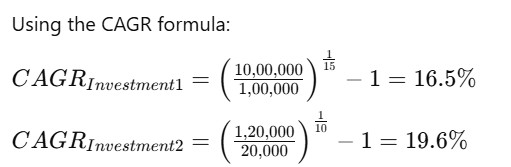

Example of CAGR Calculation

Consider two investments:

Investment 1: ₹1 lakh grows to ₹10 lakh in 15 years.

Investment 2: ₹20,000 grows to ₹1.2 lakh in 10 years.

Although Investment 1 generates more wealth, Investment 2 has a higher annualized growth rate.

Key Differences Between XIRR and CAGR

| Feature | XIRR | CAGR |

|---|

| Definition | Measures annualized return with multiple cash flows at different times | Measures average annual growth assuming a fixed return rate |

| Best for | SIPs, phased investments, and irregular cash flows | Lump sum investments with steady growth |

| Accounts for Timing? | Yes | No |

| Calculation Complexity | More complex; requires financial tools | Straightforward; can be calculated manually |

Which One Should You Use – XIRR or CAGR?

Use XIRR If:

✔ You invest through SIPs or multiple transactions. ✔ Your investments have irregular cash flows. ✔ You need an accurate measure of performance based on cash flow timings.

Use CAGR If:

✔ You invest lump sum for the long term. ✔ You want a simple and quick comparison of different investments. ✔ Your investment has a steady growth rate over time.

XIRR vs CAGR: Relevance for Indian Investors

For Mutual Fund Investors: SIP investors should track XIRR, while lump sum investors should focus on CAGR.

For Real Estate Investments: If payments and returns happen at different times, use XIRR.

For Retirement Planning: Those investing in PPF, EPF, or NPS may find CAGR more relevant for long-term planning.

For Stock Market Investments: Active traders should use XIRR, while passive investors may prefer CAGR.

Final Thoughts

Both XIRR and CAGR are valuable tools for measuring investment performance, but they serve different purposes.

If you invest through SIPs or multiple cash flows, XIRR provides a precise measure of returns.

If you invest lump sum, CAGR offers a simplified view of growth over time.

Understanding these key differences will help you track your investments better and maximize your returns. Want to calculate XIRR or CAGR for your investments? Use Excel sheets or an online financial calculator for accurate results!

By leveraging the right metric, Indian investors can make smarter financial decisions and achieve their investment goals effectively.

Disclaimer:

The views and opinions expressed by the author are for informational and educational purposes only and should not be considered financial, investment, or legal advice. SaveFundsNow does not provide investment recommendations or endorse any financial products.

Investing in financial markets is subject to market risks. Readers are advised to conduct their own due diligence, Discuss with your SEBI Regd Financial Advisor, and make investment decisions based on their own research.

SaveFundsNow and the author disclaim any liability for financial losses or decisions made based on the content provided.