Corporate Insolvency Resolution Process (CIRP)

Table of Contents

ToggleThe Corporate Insolvency Resolution Process (CIRP) is a structured mechanism under the Insolvency and Bankruptcy Code (IBC), 2016, designed to address the insolvency of corporate entities in India. It aims to balance the interests of creditors and debtors while attempting to revive a financially distressed company. If revival is not possible, CIRP ensures the maximum value realization of the company’s assets before liquidation.

This guide explains the key aspects of CIRP, including its process, documentation requirements, and impact on stakeholders.

What is Corporate Insolvency Resolution Process (CIRP)?

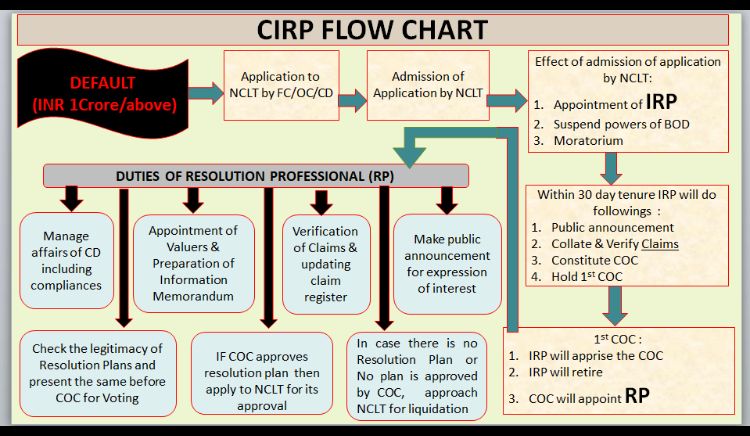

CIRP is the process by which a financially struggling company is given an opportunity to restructure its debt and operations under a regulated framework. If the resolution process fails, the company is liquidated. It is initiated when a company defaults on a payment of at least ₹1 crore (subject to change as per government amendments).

Key Features of CIRP

1. Initiation of CIRP

CIRP can be triggered by:

- Financial Creditors: Banks or lenders who have provided loans to the company (Section 7 of IBC).

- Operational Creditors: Suppliers, vendors, or service providers who are owed money (Section 9 of IBC).

- Corporate Debtor: The company itself can voluntarily admit its insolvency (Section 10 of IBC).

2. Admission by NCLT

- The application for CIRP is filed with the National Company Law Tribunal (NCLT).

- Upon admission, a moratorium is imposed under Section 14, which halts all legal proceedings, asset foreclosures, and recovery actions against the debtor.

3. Appointment of Interim Resolution Professional (IRP)

- The NCLT appoints an Interim Resolution Professional (IRP) to take control of the company.

- The IRP replaces the existing board of directors and manages the company’s affairs temporarily.

- The IRP also verifies claims from creditors and forms a Committee of Creditors (CoC).

4. Role of the Committee of Creditors (CoC)

- The CoC comprises financial creditors and plays a key role in the resolution process.

- It appoints a Resolution Professional (RP) to oversee the process.

- The CoC evaluates and votes on resolution plans, with a 66% majority required for approval.

5. Resolution Plan Submission and Approval

- The RP invites resolution applicants (potential investors, buyers, or existing promoters) to submit plans for the company’s revival.

- The resolution plan must include provisions for debt restructuring, asset sales, or capital infusion.

- If the plan is approved by the CoC and NCLT, the company is handed over to the successful applicant.

6. Timeframe for CIRP

- CIRP is intended to be completed within 180 days, with a maximum extension of 90 days (330 days, including litigation delays).

- If no resolution plan is approved within this period, the company moves to liquidation under Section 33.

Required Documents for CIRP Application

For Financial Creditors

- Record of default from an information utility.

- Details of the proposed IRP.

- Any supporting documents specified by regulatory authorities.

For Operational Creditors

- Invoice demanding payment or a demand notice sent to the debtor.

- Affidavit confirming the absence of a dispute from the debtor.

- Financial institution certificate proving unpaid debt.

- Report from an information utility (if available).

For Corporate Debtors

- Financial records proving insolvency.

- Special resolution from shareholders approving CIRP initiation.

- Details of the proposed IRP.

What Happens After CIRP is Initiated?

1. Moratorium Period

- Once CIRP begins, a moratorium stops all legal proceedings against the debtor.

- Creditors cannot take legal action to recover debts during this period.

2. Impact on Shareholders

- Shareholders may experience equity dilution as new investors take over the company.

3. Management Takeover

- The existing management loses control, and the RP assumes responsibility for decision-making.

4. Successful Resolution

- If a viable resolution plan is approved, the company can continue operations under new management.

5. Liquidation (If No Resolution is Found)

- If no resolution plan is approved, the company is liquidated.

- The proceeds from asset sales are distributed based on the priority framework in Section 53 of IBC:

- Secured creditors

- Employees and workmen

- Unsecured creditors

- Government dues

- Equity shareholders (if anything remains)

Advantages of CIRP

- Prevents Unnecessary Liquidation: Allows distressed companies to explore restructuring before shutting down.

- Time-Bound Process: Ensures quick resolution (180-330 days max).

- Creditor-Centric Approach: Ensures creditors recover maximum value.

- Improves Business Continuity: Gives companies a second chance at revival.

Challenges in CIRP Implementation

- Delays in NCLT Proceedings: Overburdened tribunals often lead to extended timelines.

- Disputes Among Creditors: Creditors may have conflicting interests, slowing the process.

- Lack of Resolution Applicants: Not all distressed companies find suitable buyers or investors.

- Legal Hurdles: Ongoing litigations and regulatory changes impact resolution efficiency.

Real-World Impact of CIRP

Since its introduction, CIRP has transformed India’s insolvency framework by reducing Non-Performing Assets (NPAs) in the banking sector. Some major cases include:

- Essar Steel Case: Led to a landmark Supreme Court ruling on creditor hierarchy.

- Jet Airways Case: Showcased challenges in reviving debt-ridden companies.

The Corporate Insolvency Resolution Process (CIRP) is a crucial mechanism under the Insolvency and Bankruptcy Code (IBC), 2016, aimed at resolving corporate financial distress efficiently. It offers businesses a chance to restructure while ensuring creditors recover their dues. However, challenges such as legal delays and creditor conflicts continue to impact its effectiveness.

Understanding CIRP is vital for businesses, investors, and financial institutions, as it directly influences economic stability and the investment climate in India.

If your company is facing financial distress, consulting an insolvency professional can help you navigate the CIRP effectively.

Disclaimer:

The views and opinions expressed by the author are for informational and educational purposes only and should not be considered financial, investment, or legal advice. SaveFundsNow does not provide investment recommendations or endorse any financial products.

Investing in financial markets is subject to market risks. Readers are advised to conduct their own due diligence, Discuss with your SEBI Regd Financial Advisor, and make investment decisions based on their own research.

SaveFundsNow and the author disclaim any liability for financial losses or decisions made based on the content provided.